Milton Keynes lies half way between Oxford and Cambridge, and is known to historians driving between the two universities for its succession of roundabouts, its concrete cows grazing beside the road, and huge distribution warehouses. If they think of history, it is Bletchley Park – the home of the wartime code breakers – that is subsumed in the new town. They hurry on to their idyllic destination with a sigh of relief that they do not live in this arid and soulless dystopia. But as Guy Ortolano shows in his outstanding book, Thatcher’s Progress: From Social Democracy to Market Liberalism through an English New Town (Cambridge Uniiversity Press, 2019) they should pause and reflect on what the development of Milton Keynes shows about wider political process in late twentieth century Britain.

Mrs Thatcher herself visited on 25 September 1979 to open Europe’s largest shopping center. After lunch, Denis Thatcher gestured to the center and remarked “Isn’t it wonderful what the private sector can do?” (Ortolano 253) – a muddle-headed response to an impressive state-funded, publicly managed development. Soon, the Thatcher government started to sell off council housing, to privatise public utilities, and to transfer public land to the private sector. Milton Keynes was no exception. Brett Christophers notes that about 18,000 acres was acquired for the construction of the new town and much of it was returned to private ownership through the government’s ‘right to buy’ public housing at a discount of up to 30 per cent. Social democracy was turned into market liberalism.

The initial idea for a new town in Buckinghamshire came from the county council and its planning officer, Fred Pooley. His vision of North Bucks New City was a new town for affluence, the motor car and modernity, with a free monorail system linking fifty or so neighbourhoods of 5-7,000 to central shops and leisure facilities. The ‘monorail metropolis’ would be planned for the motor car without allowing the car to destroy the city, and looked to Disneyland and Wuppertal. Pooley’s plans were accepted by Conservative-controlled Buckinghamshire County Council in 1964 which bought into a social democratic vision that was both inspired by and influenced international thinking. Pooley wanted to show that Britain, far from declining, could still lead the world. But his vision collided with the new Labour government elected in 1964.

Other new towns were the creatures of the central government and autocratic development corporations whose budget and membership were set in London – and the permanent secretary of the Ministry of Housing and Local Government, the imperious Evelyn Sharp, had no intention of allowing any exception. The great thing about development corporations, she insisted, was that ‘they can get on with their job without consulting public opinion’. (Ortolano 60). In 1967, control passed to a development corporation chaired by a socialist businessman, Jock Campbell, whose family fortunes came from sugar plantations in British Guiana – a different, indication of global reach. Campbell realised his fortune had been based on slavery, indentured labour and exploitation, and he aimed to redeem himself by a commitment to people over profits both in the empire and at home. The welfare state replaced the empire – and he was not alone, for ten general managers of new towns had been colonial officials. Campbell was joined by the planner Richard Llewellyn-Davies who sat on the Labour benches in the House of Lords and whose family was part of the ‘intellectual aristocracy’. Rather than Pooley’s vision of Brasilia in Buckinghamshire, Llewellyn-Davies’s vision was mini-Los Angeles – a motor city based on dispersal, mobility and open-ended planning or ‘indeterminate architecture’ of system of grids, roundabouts and parks that could be expanded in a flexible manner. His vision owed much to the Berkeley futurologist Melvin Webber who argued that urbanism must change in response to the rise in services, education, knowledge and affluence. Webber stressed that urban forms should be based on indeterminacy and networks, on ‘community without propinquity’. The planning of Milton Keynes was inspired by international thinking, and Llewellyn-Davies then took an international role for nationalised Britain. He opened an office in New York in 1967 and expanded into the middle east, above all in re-planning Tehran. And in Milton Keynes, the Development Corporation recruited modernist architects such as Norman Foster to build in ‘welfare state modernism’ of non-traditional materials and flat roofs, free from the constraints of the market.

This social democratic vision gave way to market liberalism that is captured in the shift from about 75 per cent to 25 per cent of housing being in the public sector. Ortolano shows the change was carried through by social democrats who did not necessarily change their minds but had to adjust their behaviour. Funding cuts after the IMF crisis of 1976 forced the Development Corporation to look for new ways of securing revenue – including creating a consultancy to advise on new towns in Saudi Arabia and Nigeria. Social democracy did not die; it remained dynamic in its response to market liberalism until, in the end, it internalised the priorities of market liberalism. The only way to continue the social democratic ambition was to encourage owner occupiers to come to Milton Keynes – and the only way to ensure the would-be purchasers had access to loans was to drop ‘welfare state modernism’ in 1981 for traditional, saleable housing acceptable to lenders and would-be purchasers. Architectural style reflected market liberalism, as the Development Corporation struggled to show success in the new metric of owner occupation. Social democrats struggled to succeed in the new world of Thatcherism and ‘the logic of survival transformed Milton Keynes into an avatar of market liberalism’ (0rtolano 200).

Ortalano’s book has wide implications for Britain’s post-imperial history as it struggled to find a new international role, for changes in urban form and architecture, for notions of community and affluence. It is a pleasure to read. Brett Chrisophers book on The New Enclosure: The Appropriation of Public Land in Neoliberal Britain (Verso, 2018) is more tightly defined and more engaged (even enraged). He shows that it was not only the public land of Milton Keynes that was sold – other land owned by public bodies from the Ministry of Defence to National Health Service changed hands. Although precise estimates are difficult to produce, Christophers plausibly suggests that public landownership after the Second Word War was around 12-14 per cent of the land of the United Kingdom which expanded to about 20 per cent – mainly as a result of purchases for social housing – by the time Mrs Thatcher assumed office. Since then, about 10 per cent has been transferred to private hands (Christophers, 96, 117, 248-9). This ‘new enclosure’ has led to surprisingly little scrutiny and protest, in part because it has been piecemeal, in part because it has reputedly benefitted former tenants of council houses and wider share-ownership in the privatised industries.

Christophers’ analysis lacks the subtlety of Ortolano’s nuanced account of the rise of market liberalism, but his account of the ways in which land has been transferred from public to private ownership since 1979 is compelling. His concern is not with the transfer of land as the incidental result of privatisation of, say, the National Coal Board or public utilities which accounts for about 20 per cent of the total transfer. Rather, he focuses on the privatisation of land qua land, and in particular from local authorities which accounted for around 60 per cent of the transfer, much of it through the sale of council houses. The case for privatisation of land was that the public sector had a surplus of land which was used inefficiently, and that if it were transferred to private owners, they would build more housing and encourage economic growth. Christophers shows that these propositions were not tested against land use by private owners, or by different criteria of social use than profit. Many councils did not wish to sell, or public owners might prefer to transfer land between themselves to meet the demand for new hospitals or schools or housing. Christophers convincingly shows how the central government closed down options by setting space utilization targets, creating registers to identity ‘surplus’ land, devising accountancy methods that gave public land a market value that prioritised sale, and then introducing constrains and incentives that made sale to private owners virtually certain.

The transfer has not had the promised desirable consequences of additional housing or growth. In Milton Keynes, 71 per cent of council apartments sold to tenants passed to private landlords, the highest rate in the country – and tenants of private owners receive more housing benefit than in the denuded social housing sector. The state now spends about twenty times as much on housing benefit as it does on building affordable social housing. The transfer of social housing to tenants did at least provide some benefit to workers: as Massimo Florio showed in The Great Divestiture: Evaluating the Welfare Impact of the British Privatizations 1979-1997 (Cambridge Mass 2004), it was the only privatization with any claim to have a progressive impact on distribution. He found no evidence that privatization benefited the consumer, workers or the taxpayer; the gains went to shareholders as a result of under-pricing and out-performance (in contrast to most public offerings which are over-priced and then under-perform) and to managers and financiers. Christophers finds a similar outcome in land transfers which have benefitted large property firms that are hidden behind opaque corporate structures. By contrast to the pressure on public owners to make their ownership transparent, the ownership of private land can only be discovered by assiduous investigative journalism such as Guy Shrubsole in Who Owns England? How We Lost Our Green and Pleasant Land and How to Take it Back (2019).

Christopher is writing in the tradition of great historians such as R H Tawney and E P Thompson on the seizure of monastic land and the enclosure of the common fields – something for our historian to contemplate as she navigates the roundabouts in Milton Keynes. And she should no deride the cows as she proceeds between the two universities. The Development Corporation aimed to build community as newcomers arrived, above all from inner London. The social development department met new arrivals with a cup of tea and a friendly face, and also embarked on ‘animation’. In 1977, Jack Trevor arrived as the first creative writer in residence, and animated the scene by suggesting the town need a creative psychiatrist, and that his aim was ‘to corrupt students’ so that imaginative four-year olds were not turned by the educational system into ‘pricks’. (Ortolano 167). Less abrasive was his neighbor Liz Leyh, the first artist-in-residence who arrived from New York. Children joined her in animating the new town with a huge giraffe, an installation inspired by the Wizard of Oz, concrete snowman, hippopotamuses, ice-cream cones – and of course, the cows that were her parting gift to the town. Her aim was ‘to define community arts as the participation of an artist with other people or an art form which enables different people to participate with each other’ (Ortolano 169). The cows now inspire derision from passing motorists who do not understand the cultural world in which they were created. Ortolano’s brilliant book allows us not only to grasp that cultural world, but more generally to appreciate how the construction of Milton Keynes illustrates fundamental changes in British society that allowed Dennis Thatcher’s mistake to be taken as truth.

http://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.png00Martin Dauntonhttp://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.pngMartin Daunton2020-12-29 14:10:032020-12-29 14:11:37Milton Keynes to Milton Friedman

A previous lecture delivered in Melbourne in May 2019 dealt with Brexit in the longer term – how relations with Europe changed since 1945, from ambivalence to membership and back to ambivalence. In this lecture, also in Melbourne, in November 2019 I turned to some major issues which have been opened up and need to be resolved

THE MEANING OF DEMOCRACY

A referendum is a form of plebiscitary democracy that is not

easily reconciled with representative democracy.

Until 1970s, a referendum was thought unconstitutional

because parliament was sovereign. The constitutional

lawyer AV Dicey argued in the later nineteenth century that judges know nothing

of the will of the people except as expressed in an act of parliament.

How is a decision reached on what is an appropriate issue

for a referendum? One view is that is

should only be used for a constitutional issue, which begs the question of what

is the constitution? In reality,

referenda have been used for tactical reasons related to party discipline, and

not really to show the will of the people.

When used, referenda could therefore only by advisory and

not binding – though in 1975 and 2016 executive decided that they would be

bound.

Referenda can work for a binary choice. I have recently experienced

three: one is the referendum on the EU in 2016, and the others were

Australia

2017: same sex marriage, yes or no

Switzerland

2018: should cows have their horns removed, yes or no

A simple binary vote was inappropriate for membership of EU,

for there was no clarity over what ‘leave’ meant. The choice was likened to vote: yes or no to

the question ‘shall we go to the cinema’.

When ‘yes’, a choice then has to be made whether the film is The Sound

of Music or The Texas Chain Saw Massacre.

An appeal was made to the ‘will of the people’ which MPs were

meant to carry out – even if that was true, how was one to interpret what the

‘will’ actually is? And is it the

overall vote (52 per cent leave) or that of the individual constituency or – very

importantly since devolution – the constituent nations of the United Kingdom?

Take the case of Dominic Grieve, the MP for Beaconsfield, a

leading supporter of membership and former Conservative Attorney General. To some, he was a ‘traitor’ for going against

will of people – but his own constituency voted 51 per cent remain. In any case, Edmund Burke is buried in Beaconsfield

churchyard, and he informed the voters of Bristol in 1774 that an MP was not a

delegate but a representative or trustee who served the public or national

interest: “his unbiased opinion, his mature judgment, his enlightened

conscience, he ought not to sacrifice to you, to any man, or to any set of men

living. … Your representative owes you, not his industry only, but his

judgment; and he betrays, instead of serving you, if he sacrifices it to your

opinion”. A trustee exercises his own judgment in making decisions about

what should be done. “You choose a member, indeed; but when you have

chosen him, he is not member of Bristol, but he is a member of

Parliament”.

Referendum mean setting this principle aside.

Another issue is the time scale for a referendum. Calls were made for a second referendum on

two grounds:

We would not know what sort of leave would be

offered until a deal was negotiated. One

would not buy a house if the survey found it had serious flaws; and a trade

union would put a deal to a vote after a strike

The electorate changes: younger and more

educated larger share of electorate, more in favour of remain

The view that the ‘will of the people’ can only be expressed

is in tension with democracy as a process in which the losing side can continue

to campaign. This disagreement is very

deep and dangerous. It also led to

hypocrisy, for Nigel Farage of UKIP said that if he lost 48/52 he could

continue to fight; when he won 52/48, calling for a new referendum was

treachery by bad losers.

Referenda are a sign of failure to handle complex political decisions. Difficult issues should be resolved by handling complexities with a continuum of views that are argued out within parties and parliament to reach a compromise that few would choose as their preferred option but which the largest number can accept as tolerable. Parties traditionally played this role as mediators between the state and citizens. Referenda stop this process and by-pass the political process of politicians accommodating the widest range of opinions by giving it to individual electors who have no reason to consider any opinion except their own, and which leads to a stark divide in which 48 per cent are no longer the British people but are portrayed as enemies/traitors/saboteurs. As one member of the public said on television, the vote on 23 June 2016 was clear and there should be no remainers left. In the opinion of Jonathan Sumption, the former judge on the Supreme Court, ‘This is the authentic language of totalitarianism. It is the lowest point to which a political community can sink short of actual violence’. More immediately, such views created difficulties for parliament as it turned to the messy business of compromise which was blocked by the outcome of the referendum.

THE CONSTITUTION

The British constitution is unique, for it is not written

other than eight words: ‘whatever the Queen in parliament enacts is law’. It is historical and not legal. There are no constitutional limits on the power

of parliament which is sovereign; the exercise of powers is a matter for

ministers answerable to parliament and ultimately to the electorate. There is no fundamental law that parliament

cannot repeal or alter at will. Is this

dangerous and open to abuse, for it relies on conventions which can be broken –

or is it a source of flexibility? We should

also note that English and Scottish parliamentary sovereignty are different: prior

to the Act of Union of 1707, the executive in Scotland was not accountable to

parliament so why should the united parliament of Great Britain only accept the

English principle?

Joining the EEC/EU did set a higher body above parliament

and in that sense the Brexiteers are right.

It was not really considered at the time, but it was apparent after 1991

that there was a shift from a historic to a legal constitution. Does it matter?

To some, it matters a lot: continuing

sovereignty means that a sovereign body cannot bind itself

To others, it does not mattera lot: self-embracing

sovereignty means a sovereign body can agree to bind itself.

Arguments over the ‘will of the people’ can lead to a claim

that the people are against the courts and against parliament. There were two

legal challenges to the role of the executive:

The decision of three judges that parliament

needed to vote to trigger article 50 (for departure from the EU) and could not proceed

simply by the executive sending a letter.

A Daily Mail headline 4 November 2016 called them ‘Enemies of the

People’.

Whether Prime Minister Johnson misled the queen

in proroguing parliament in September 2019: the High Court in England ruled it

was a political decision and permissible; the court in Scotland found it was

misleading advice. The Supreme Court of the

UK ruled against Johnson and stated that the act of prorogation never happened.

Both judgements cited cases going back to Charles I and

civil war and raised serious constitutional issues:

What is ‘justiciable’? What is the line between a political

decision/judgement and what the courts can decide? Sumption argued prior to the case that judges

had been intruding into political issues: they are unelected and unaccountable,

and should not intrude on political decisions which are, as we said earlier,

about reaching compromises. But the

night before the decision on prorogation, he remarked on BBC that Johnson had

taken a hammer and sickle to the constitution, and it was justiciable issue.

What is the role of the monarch? Sovereignty was vested in sovereign until 1688/9

when rules were introduced to limit the power of the monarch over parliament. The issue now is that the monarch has no

authority to take an independent judgement over executive and merely does as

executive says, as happened when the queen accepted prorogation until it deemed

never to have happened by the Supreme Court.

These issues are now open:

What form should the constitution take?

Is the solution a written constitution? Dominic Grieve thinks so. It would clarify the role of judges;

conventions only work if they are followed and not broken. Can we have a constitutional court as in

Italy (15 judges for 9 years, 5 appointed by president, 5 by parliament and 5

by judges)?

Or will it lead to inflexibility as in US? The unwritten constitution in the UK can

handle unexpected issues – a written constitution gives more power to unelected

judges and hampers the process of finding compromises. In US, the Supreme Court makes law by the use

of the Due Process clause of 14th amendment which can be used

illiberally (for example, to stop collective bargaining) or liberally (for

example, to approve abortion which has never been legislated on as in UK).

A political constitution is better than a legal

constitution.

What is power of head of state? Queen cannot express her own view, unlike president in Italy (as in recent decision over snap election) or Germany. The monarchy is likely to survive – in which case, should there be a constitutional court in place of the Privy Council?

The House of Lords is the largest second chamber in the world and is not elected (with the oddity of hereditary peers electing some of their number). The remainder are appointed by the PM. Would something like the German Bundesrat or federal council work, which has representatives of 16 Lander?

The failure of parties to reach compromises through the political process reflects a decline in membership from the post-war period when there were about 3m members of the Conservatives, a million individual members in Labour plus affiliated unions. Boris Johnson was effectively chosen as PM by 150,000 untypical Tory members voting on their leader. Possible solutions:

Proportional representation to give more voice to small parties so not excluded; encourage process of finding compromises. Almost came in 1918; the UK is now the only European country with first past the post elections.

Open primaries for the choice of candidates so that it is not left to a small number of members and entrists. Some Conservative candidates were chosen in open primary by all electors: Sarah Wollaston in Totnes was not even a party member (though she later defected to the LibDems).

DOES THE UNION HAVE A FUTURE?

I think the answer here is that it does not unless a new settlement is reached.

There is an Irony that the Conservative and Unionist Party

might lead to a destruction of the Union.

Let’s consider the situation in Ireland.

The Good Friday Agreement of 1998 is de facto part of the

constitution of the UK like the bill of rights of 1689. Now there is tension between leaving the EU

and commitments in the agreement. Tony Blair,

one of the architects of the agreement, has said that “It is a shame and an

outrage that peace in Northern Ireland is now treated as some disposable

inconvenience to be bartered away in exchange for satisfying the obsession of

the Brexiteers with wrenching our country out of Europe”.

In the 2016 referendum, the issue of the relation of Northern

Ireland with the republic of Ireland was not given much attention, and if

mentioned was dismissed as trivial. It

turned out to be the major stumbling bloc that reflected a lack of understanding

of both history and simple economics.

Astonishingly, Karen Bradley, the Secretary of State for Norther

Ireland in 2018/19 commented that ‘I didn’t understand things like when

elections are fought, for example, in NI – people who are nationalists don’t

vote for unionist parties and vice versa’.

She then added that killings by the army and policy were not crimes,

during the hearings on Bloody Sunday when the army fired on a crowd.

There is also the issue of the customs union: there are no

tariffs on goods within the customs union, and a single common external tariff

against the outside world. The Norther

Irish/Irish border then becomes a customs line, yet the Good Friday agreement

says that the island of Ireland is to be a single economic unit. Goods could enter Northern Ireland at

potentially lower tariffs than levied by the EU (or with different phytosanitary

standards) and move into EU via Ireland; could hormone injected beef from US which

is banned in the EU secure access? Boris

Johnson simply swept the issue aside.

But thee is a serious issue that when the UK leaves the customs union, a

hard border will be needed with Ireland that

breaches the Good Friday agreement. The

solution in Teresa May’s deal was a backstop which potentially keeps UK within

customs union so that it would not be able to strike its own trade deals and regulatory

standards. It was rejected. The alternative is a border down Irish Sea

which is not accepted by the Democratic Unionist Party since it cuts NI from

the rest of the UK.

The Northern Ireland Act, 1998, obliges the secretary of

state to call a border poll ‘if at any time it appears likely to him that a

majority of those voting would express a wish that NI should cease to be part

of the UK and form part of a united Ireland’.

How is the secretary of state to decide? Is it a majority in opinion polls; a Catholic

majority in census; a nationalist majority in the Assembly; or a vote by the

Assembly?

If the referendum is called, a referendum must be held in the

Republic on the same day on unification; and if both passed, a second referendum

is needed in the Republic on an amendment to the Irish constitution. What happens if the votes differ?

Then there is the issue of Scotland where pressure exists for

a second referendum on independence. Why should Ireland have ability to remain de

facto in the customs union and not Scotland?

A prediction is that unification of Ireland is very likely

and independence for Scotland is possible.

Regardless of what happens, the existing levels of devolution in Northern

Ireland, Scotland and Wales means that England constitutionally does not exist.

Local government is complicated and dysfunctional. There is a sort of quasi-devolution to mayors

in Greater London Authority and Greater Manchester, but it is all ad hoc. Could there be regional assemblies which

could then create something like the Bundesrat?

England is the only part of the UK without a separate voice. The West Lothian question of Tam Dalyell has

not been answered: an English MP cannot vote on health care policies in West

Lothian, but a Scottish MP can vote on health care policies in West Bromwich.

A new act of union is needed for a federal system

ECONOMIC RELATIONS

The issue of the customs union arose over Northern Ireland

and the issue still remains unresolved over what sort of trading environment

should be adopted.

One view is that close alignment is needed

because of integrated supply chains in the car industry; logistics of

drugs/food – most trade is with Europe.

The alternative view is that freedom outside

customs union is needed to make trade deals in a free buccaneering spirit with

growing economies. The suspicion of

opponents is that it is about deregulation – trade deal with US mean

chlorinated chicken, hormone injected beef, weaker environmental or labour

standards; threat to NHS.

There are problems here:

Constitutional issues: phytosanitary standards are devolved to Scotland and Wales, so they could refuse to accept chlorinated chicken even if it was agreed in trade deal with US.

Trade on WTO rules is seen as the solution – but the UK needs to secure a seat apart from the EU [it did in February 2020]. And why should a country of 66m be able to strike a better deal than a bloc of 508m? The EU-Canada deal took 5 years and the UK is a more complex economy.

Problems are already apparent:

A fall in inward investment.

Threats to integrated supply chains

Hit to universities in loss of European Research

Council grants

Costs of additional paperwork calculated by HMRC

as £15bn [gross saving from leaving by Brexit supporters put at £18bn]

Lack of attention to services/passporting rights

– what mean for financial services?

CONCLUSION

The real issues in 2016 did not relate to membership of the

EU and Brexit but to genuine grievances which must be addressed – the rise in

inequality, growing precarity for many workers, the impact of deindustrialisation

and austerity. Leaving makes solving these

problems more difficult. Brexit was an

answer to the wrong question – how to deal with people who were genuinely

aggrieved.

We do need a long hard look at constitutional arrangements

which require high level of statesmanship.

Talk of ‘getting Brexit done’ was likened by one female

journalist as saying ‘Let’s get child-birth done’ in order to return to sleep, reading

novels, and going to the cinema. But

like motherhood, it is just the start of negotiations of the details, with

another deadline at the end of 2020.

Four years after the referendum, much remains uncertain.

http://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.png00Martin Dauntonhttp://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.pngMartin Daunton2020-07-09 15:42:472020-07-14 19:12:38The future of the United Kingdom after BREXIT

Black Lives Matter has focussed on the removal of visible markers that celebrate slaveowners in London and Bristol. But there is also another pressing need: to make visible what is currently hidden. The ways in which slavery and its ill-gotten gains permeated British society needs to be addressed and admitted.

In the Cambridgeshire countryside, near Newmarket, the estate and house of Chippenham Park opens its gardens to the public to admire the display of spring flowers, and it is a popular venue for weddings. The website of the property says that ‘in 1791 the estate was bought by John Tharp, a hugely successful sugar baron’. A visitor might consult the entry in Pevsner to be told that ‘the village is exceptionally rewarding. It is what is known as a model village, that is planned in its main features’, with its semi-detached cottages and long gardens that were constructed around 1800. We are told that Tharp rebuilt the main house and that his lake survives. The display board outside the parish church informs the visitor about the cottages and about the village school that was built in the eighteenth century.

The mention of ‘sugar baron’ is a hint of where the money came from. John Tharp was, in the opinion of Trevor Burnard, the leading historian of Jamaican planters, ‘the largest slaveholder ever known to Jamaica’ (Mastery, Tyranny and Desire, 2004). Tharp died in Jamaica in 1804, and when slavery was abolished in 1833, his heir received compensation for ten estates on the island with 2,375 slaves, as indicated on the UCL’s Legacy of British Slave-ownership database. The residents of the model houses, and visitors to the seemingly idylic English village, were beneficiaries of brutal exploitation of enslaved people who are now rendered invisible.

Restitution should not only entail the toppling of statutes; it should involve a shameful realisation of how the spoils of slavery permeated British society.

http://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.png00Martin Dauntonhttp://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.pngMartin Daunton2020-07-09 10:09:272020-07-09 12:12:09Slavery and silence

Although

the policy response to the global financial crisis prevented a repeat of the

great depression, it left the global economy in a fragile state. How would it cope with the next shock that was

anticipated to arise from a renewed debt crisis in emerging markets, financial

difficulties in China, or tensions within the eurozone? The unexpected external shock from the

coronavirus brutally exposed the lack of resilience in the global economy a

decade after the financial crisis. The

policies adopted, and approaches ignored, after 2008 continue to resonate, and the

financial crisis remains central to understanding the economic shock of the

pandemic and the policy response that should follow. The policy adopted after 2008 arose from the success

of fiscal conservatives in blocking the brief period of fiscal expansion which

had serious economic consequences over the next decade; and the policy debates

that raged then will be repeated as the world emerges from the pandemic. Can the same mistakes be repeated and steps

be taken to correct the economic weaknesses?

The coronavirus exposed the differential impact of mortality by age, ethnicity, and deprivation that arose from growing inequality of income and wealth, the insecurities of precarious employment, and the erosion of public services. These trends were apparent before 2008 as deindustrialisation led to a loss of relatively secure jobs for workers without formal educational qualifications, and ‘intangible’ capital benefitted workers with formal credentials.[1] These structural changes led to discrepancies in income and wealth, and reduced resilience, which the policy response to the global financial crisis did nothing to mitigate and much to exacerbate.

This outcome was not preordained. When the G20 met in London in 2009, Gordon

Brown, the British prime minister and host, called for a fiscal response. He was opposed by Peer Steinbrűck, the German finance

minister, who criticised Brown’s ‘crass Keynesianism’ for ‘tossing around

billions’ that would burden future generations.

At home, Mervyn King, the Governor of the Bank of England, exceeded his

authority in rejecting a fiscal stimulus: it would increase the size of the

deficit and boost consumption, so hindering the long-term need for British and

American economies to save and invest, to reduce household and bank debt, and

to resolve the trade deficit by shifting from domestic spending to exports. He

insisted that ‘monetary policy should bear the brunt of dealing with the ups

and downs of the economy’, and that was what happened.[2]

The case against fiscal

stimulus and deficits was justified by Alberto Alesina who argued that reducing

the deficit by an increase in high taxes would be ‘deeply recessionary’ and

that taxes would continue to grow as a result of automatic, inflation-linked

entitlements. By contrast, cuts in

spending would be more successful in reducing the deficit, removing

uncertainty, restoring confidence, encouraging investment, and avoiding an

unfair redistribution between present and future generations. Gains from private consumption and investment

could be larger than cuts in government spending and would therefore lead to

higher output.[3] Similarly,

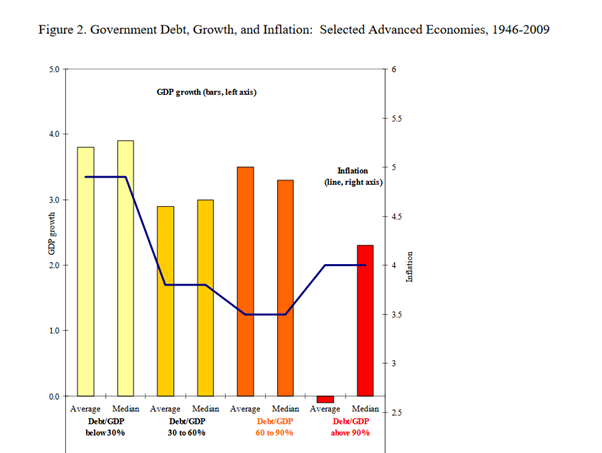

Ken Rogoff and Carmen Reinhart argued that data from 44 countries over 200

years showed that a ratio of national debt to GDP above 90 per cent reduced

growth by 2 per cent.[4] Politicians on the right, such as George

Osborne, seized on the ’90 per cent rule’ to argue that an inexorable rise of debt

threatened low growth and national bankruptcy.

Osborne duly embarked on a policy of austerity when he became Chancellor

of the Exchequer in the British coalition government in 2010.

These economic arguments

were flawed. Alesina ignored the

distributional consequences of tax increases versus spending; he overlooked the

fact that current spending can leave more assets for future generations; and he

neglected the harm of austerity on both young adults unable to secure work and the

elderly whose mortality increased. And was

it really the case that private consumption would increase when many workers

were experiencing economic hardship?

Much depended on circumstances. A cut in

public spending to balance the budget might lead to growth if debt, interest

rates and taxation were all high (as they were in Italy in the 1980s and

1990s), but not necessarily in other circumstances.[5] Oliver Blanchard and Daniel Leigh of the IMF found that a reduction in

spending or tax increases of one Euro would reduce GDP by almost 2 Euro and not,

as previously estimated, 0.5.[6] Austerity and tax increases after 2010 therefore

reduced GDP and drove economies into recession; unemployment rose and households

had less to spend, and the short-fall was not taken up by the government. As growth fell, so the ratio of national debt

to GDP rose from what it might otherwise have been. Fiscal expansion would have been a sensible

option.

Similarly, the supposed relationship

between growth and national debt was bad history. Reinhart and Rogoff lumped countries and

periods together regardless of circumstances, and their ignorance of context offers

a warning when attention turns to the higher levels of debt after covid-19. The case of Britain since the eighteenth century

shows that their ‘rule’ was misguided. Peaks

in debt arose from warfare in the Napoleonic and world wars, and the way that

debt was subsequently reduced differed. After

1815, the reduction of national debt from over 200 per cent of GDP to around 25

per cent by 1913 was largely the result of economic growth; by contrast,

inflation had no role in reducing the real burden, for prices were no higher at

the close of the period. There was also an initial period of political

unrest over the burden of the debt, for war-time income tax expired in 1816 so

that the cost of debt service came from taxation of producers and workers, with

a transfer to landed aristocrats and rentiers.

During the First World War, debt again rose above 200 per cent of GDP. Now, growth was less significant for the

economy experienced a decade of low growth as a result of the collapse of the

global economy, adoption of high interest rates to bolster sterling in

preparation for a return to the gold standard at an overvalued rate, and the

emergence of competition which led to over-capacity in major industries. ‘Financial repression’ was not an option –

that is, low interest rates and diversion of savings into government funds by

capital and exchange controls – for the government’s strategy was to maintain

open international financial markets. The

costs of servicing the debt was high and falling prices after the post-war boom

held up the ratio of national debt to GDP.

Nevertheless, the high costs of servicing the national debt was met by ensuring

that the tax regime was perceived as equitable between classes and interests. A similar level of debt after the Second World

War coincided with rapid economic growth stimulated by war demand and

facilitated by recovery of the global economy because of cooperative

action. The cost of debt service was

reduced by low interest rates and financial repression that was now permitted

by exchange and capital controls, and was paid from taxation

that shifted income to poorer members of society which created greater equality

of income and wealth, and increased consumption. At the same time, inflation contributed to

reducing the debt burden: about 30 per cent of the fall in the debt ratio to

2008 was a result of growth and the remainder from inflation.[7] The political economy of debt and its

relationship with growth therefore depended on circumstances – and this point

needs to be recognised in dealing with the costs of covid-19 when the arguments

used to justify austerity after the global financial crisis might return.

Although a selective reading of

economics provided intellectual justification for opposition to fiscal

expansion, the policies were pursued for other reasons. Mark Blyth, a leading

critic of austerity, explained that the politics of debt became a morality play

that ‘shifted the blame from the banks to the state. Austerity is the penance – the virtuous pain

after the immoral party – except it is not going to be a diet of pain that we

shall all share. Few of us were invited

to the party but we are all being asked to pay the bill’. The rhetoric of austerity shifted blame from

the banks to a bloated and inefficient public sector and overly generous

welfare.[8] On

this view, it was a cynical tactic of ‘bait and switch’. Paul Krugman commented that the rejection of

fiscal expansion was ‘the victory of an orthodoxy that has little to do with

rational analysis, whose main tenet is that imposing suffering on other people

is how you show leadership in tough times’.[9] In

both the great depression and global financial crisis, house prices in the

United States fell by a third from peak to trough; in the former, mortgagees

were assisted by the federal government and banks were regulated; in the

latter, state intervention was presented as a problem rather than cure (despite

a massive state bailout of bankers).[10] The political economy of fiscal orthodoxy in Germany

had a different rationale, for taxpayers would not do for southern Europe what

they had done for East Germany after reunification. Merkel was also concerned that the German –

and European – population was ageing so that the crucial issue was not to boost

domestic demand which would undermine competitiveness and pass the burden to

future generations. The solution was to

export and accumulate a surplus. In

2009, the Bundestag adopted a constitutional amendment to impose a rigid fiscal

rule.[11]

Both Britain and the United States, which

initially adopted a fiscal stimulus, now changed their approach. At Toronto in June 2010, the G20 announced a

commitment to ‘growth-friendly fiscal consolidation’ and argued that ‘failure to implement

consolidation where necessary would undermine confidence and hamper growth.

Reflecting this balance, advanced economies have committed to fiscal plans that

will at least halve deficits by 2013 and stabilize or reduce government

debt-to-GDP ratios by 2016’.[12] The rejection of fiscal expansion had

serious consequences that continue to resonate.

Merkel and Schauble adopted a rigid stance during the crisis of the

eurozone: no budget deficits, no common European debt issuance and no European

fiscal union. The result was slow recovery

and serious austerity in southern Europe, with a risk that when the next crisis

arrived the fundamental issues of the eurozone had not been resolved. The commitment to reducing public debt intensified the recession, whereas a

fiscal stimulus would have allowed more investment in infrastructure and

compensated for the reduction in consumption.

The policy adopted in the United

States and Britain, and eventually in the European Union, had serious

distributional consequences that contributed to the fragility of the economy in

2020. Quantitative Easing was necessary

to prevent the collapse of the financial system but exacerbated other problems. It led to higher asset prices that benefitted the richest 10 per cent or

so; their assets and income rose in an upward spiral and they had a lower

propensity to consume. The result was a savings

glut of the rich. In contrast, austerity

– as well as economic change that led to greater precarity – meant that the

lower 90 per cent of the income distribution turned to private debt and

‘dissaving’ to maintain consumption. As

their debt rose, so they had greater difficulties in maintaining their spending

with the result of economic

fragility – and the government did not step in with sufficient public spending

to maintain consumption.[13] In the New Deal and Second World War, taxation contributed to reduced inequality

of income and wealth; after the global financial crisis, corporation taxes were

reduced and disparities continued to grow with resentment and disillusion that

fed into populism and economic nationalism.

The imbalance was also apparent in

China whose economic development rested on unusually high savings and a low

level of household consumption, as a result of low interest rates, regressive

taxation, a need to supplement weak welfare provision, and gains by the party

and business elite. Before the global

financial crisis, the savings fuelled domestic investment and the current

account surplus, with funds flowing into the United States to fuel the subprime

market. After the crisis, China provided

a massive fiscal stimulus which prevented another great depression. ‘Keynesianism

with Chinese characteristics’ involved local and regional governments embarking

on ambitious schemes for investment in the infrastructure. Domestic consumption was encouraged by

subsidies to rural households to purchase large domestic appliances. The result was the largest single stimulus to

the world economy.[14] China’s fiscal stimulus prevented the recession from being any deeper

but distorted investment and created a fragile shadow banking system with a

high level of non-performing loans. Household consumption remains low, with a

continued savings glut – but without profitable opportunities for investment. The outcome could be a further round of

wasteful investment based on credit with a risk of financial crisis; the export

of goods with a massive external surplus that will cause tensions with the

United States; or a shift of incomes to boost consumption by poorer households

that will require a major change in policy.

The other major saver was Germany,

where household consumption was stagnant before the global financial crisis, the

government held down its spending, and the economy produced a large external

surplus. The outcome was lending to the

United States to fuel subprime mortgages and to other countries in Europe –

Greece, Spain, Italy – to create unsustainable credit and consumption. The response to the eurozone crisis did not

help, for Germany did not boost its own consumption and enforced austerity on other

members of the eurozone. The foundation

flow of the absence of a

fiscal union alongside monetary union was not addressed. Fiscal

transfers needed to be higher in Europe because labour mobility was lower than

in the United States; in fact, transfers were much lower. In February 2020, the so-called ‘frugal four’

of Austria, Denmark, Sweden and the Netherlands aimed to limit the EU budget to

1 per cent of GDP compared with their own revenues of 48, 52, 49 and 44 per

cent of GDP. This ratio of 40 or 50 to 1

between state and federal revenues contrasted with a ratio in the United States

of 1 to 2 between state/local and federal spending. A much larger European Union budget is needed

to deal with structural change, environmental sustainability, education, health

care and research and development, at a time when inequalities between regions

cause strain.[15] This approach was anathema in Germany which

tried to extend its own fiscal conservatism to the rest of the EU.

When covid-19 hit, the problem of the savings glut had not been

resolved: it existed before the global financial crisis, and the policy

response had done nothing to resolve the problem either within individual

countries or in the imbalance between global savers and debtors. The major question is whether the crisis of

covid-19 can allow an escape from the problem of the savings glut and low

consumption that was not taken after the global financial crisis?

Despite austerity, automatic payment of welfare

benefits and low growth meant that national debt rose in most OECD countries after

the financial crisis. In France, it

increased from 87.8 per cent in 2011 to 98.4 per cent in 2018, in Italy from 119.7

to 134.8 in Italy, in the United Kingdom from 80.1 to 85.7, and in the United

States from 99.8 to 106.9. The exception

was Germany where the level fell from 79.8 to 61.9 per cent. Debt levels were

already high before covid-19 and are set to rise closer to war levels. In April 2020, the IMF’s tentative initial

estimate was that by 2021 the debt to GDP ratio would rise to 116.4 per cent in

France, 150.4 per cent in Italy, 95.8 per cent in the UK, 131.9 in the US but only

to 65.6 per cent in Germany. [16]

The figures are estimates whose

accuracy will depend on the trajectory of the pandemic, the speed of recovery,

and political choices.

Many commentators, politicians and economists now accept that

rejection of fiscal expansion after 2010 resulted in weak public services and contributed

to the disparities of the virus. On the

other hand are those who argue that the level of debt is unsustainable and that

it will exacerbate the generational divide of the pandemic. Why should the younger generation be left to

pay for high levels of debt when their prospects are employment are reduced and

growth might be suppressed? Adam Tooze rightly thinks

that the question of repayment ‘will decide the complexion of our politics, and

the quality of our public infrastructure and services for years to come’ He fears that the level of covid debt can be a

‘battering ram’ for a new campaign of austerity and ‘conservative

scaremongering’.[17]

In April 2020, Gordon Brown reflected on his failure to sustain the case for

fiscal expansion after 2008, and called for his successors to avoid making the

same mistake again.[18]

Although the generational divide

is serious, the solution is not a return to austerity to reduce debt. The real burden of debt can be reduced by

moderate inflation as after 1945. The (largely

unjustified) fear of inflation led to caution in stimulating demand after the

financial crisis. Of course, rapid

inflation as in Germany in the early 1920s created social dislocation and

resentment as fixed incomes and savings were eroded. Equally, the pursuit of price stability since

the late 1970s benefitted creditors and increased the real burden of debt. The solution is a careful calibration of

central bank intervention to allow a modest level of inflation that can, as

after 1945, gradually reduce the level of debt and stimulate consumption.

The cost of servicing the debt then needs to be held down, as

it was by low interest rates and financial repression after 1945. The policy became mor difficult with the

resurgence of international capital markets and financial flows from the 1970s,

but Quantitative Easing has led to a decade of low interest rates that is not

likely to be reversed soon. It is not only a policy choice by central

bankers but a structural issue: the savings glut of the rich led to downward pressure

on interest rates to balance the supply and demand for savings. The risk of

higher rates can be reduced by extending the duration of bonds or making them

perpetual. It is therefore possible to

live with the larger national debt, provided that annual deficits are reduced enough to stabilise

its level – and this can be achieved by increases in taxation rather than cuts

in spending.

Low interest rates and the glut of savings are not without problems, for they reflect large disparities of income and wealth that have been exacerbated by rising assets prices created by quantitative easing. The economy was vulnerable prior to the pandemic because of high levels of household and corporate debt which led to the global financial crisis and continued afterwards. The focus on public debt distracted attention from the real problem: an increase in household debt to maintain consumption and in corporate debt to fund stock buybacks, embark on mergers and acquisitions, increase profits, and pay higher dividends. Indebtedness rose in line with inequality. What was needed after the global financial crisis, and could be achieved now, is a set of policies that creates greater equality to remove the savings glut of the rich, so allow consumption to rise without the need for higher levels of household debt, and removing the incentive for corporate leverage.

This change could encourage economic growth which was the main reason

for the reduction in the level of the national debt after the Napoleonic wars

and a major cause after 1945. Excessive fiscal consolidation after

2010 reduced growth and damaged productivity and made the debt burden worse. American and European economies suffered from

low growth and stagnating productivity and the policies adopted after 2008 failed

to provide solutions to low growth and stagnating productivity in the United

States and Europe and might have made matters worse. The rebalancing of economies might stimulate

investment and growth and remove risky reliance on corporate debt to maintain

profits and household debt to maintain consumption. Of course, redistribution and the removal of

the savings glut might lead to higher interest rates and an increase the costs

of servicing the national debt in the longer run, but in the short to medium

term low interest rates can be locked in as the debt ratio is reduced by faster

economic growth.

Faster growth will mean changing the tax regime. In some countries, the level of taxation is

low which provides more fiscal headroom to raise taxes rather than cut spending:

the level of taxation as

a share of GDP in France is about twice that of Ireland which therefore has

more fiscal headroom. But the issue is

not only the level of state revenue, for the structure of taxation and

perception of fairness are also important, as we noted at the end of the Napoleonic

wars in Britain. Tooze correctly comments

that ‘who pays taxes – and who does not – remains one of the most urgent

questions of the moment. A world in

which coronavirus debts are repaid by a wealth tax or a global crackdown on

corporate tax havens would look very different from one in which benefits are

slashed and VAT is raised. And it is

very possible that debt service will be taken out of other spending, whether

that be schools, pensions or national defence’.[19] What tax regime will permit faster growth and

encourage productivity?

A redistributive strategy to remove the savings glut of the rich and

transfer consumption to the rest of society will require a major shift to a

more progressive pattern of taxation and spending in the United States on the

lines of the New Deal; and a return in Britain to something more like the

pre-Thatcher period. In China, it will require

greater benefits for migrants from the country to the town, improved welfare

benefits and workers’ rights, and a shift in taxes to the rich. Abolishing tax deductibility of corporate

debt could discourage a reliance on financial leverage. Action could be taken against multinational

corporations who erode the fiscal base by shifting their profits to low tax

regimes – and taxes could be introduced on the rent-seeking behaviour of digital

and tech companies. A wealth tax could capture the gains of rising assets from Quantitative

Easing and break the upward spiral of inequality. ‘Green’ taxes on carbon and congestion would

ensure that growth did not come at the expense of the planet. The revenue from higher or restructured taxes

could then be spent in ways that encourage an economic transformation by giving

incentives to green technology, better education and training, and improved physical

and social infrastructure to regenerate declining industrial areas. The failure to tackle these issues after 2008

contributed to the economic fragility and populism that hindered the response

to the pandemic.

None of these changes will be easy, but they are not impossible. The Chinese Communist party’s main aim is to maintain social order and power, so a shift in its policy is not implausible – and the outcome n the United States might change with the demands of younger members of the Democratic party. There are also signs of change in the European Union away from the refusal of Germany to transfer resources or to stimulate domestic consumption that limited the response to the crisis of the eurozone. Concern about the bond purchasing programme of the European Central Bank was raised in the German constitutional court and passed to the European Court of Justice which supposed the policy. The issue was returned to the German constitutional court which decided in May 2020 to reject the ECJ’s judgement – a potentially devasting blow to the ECB’s response to the pandemic that caused outrage in Spain and Italy. The decision was economically perverse but the court’s defence was that it interpreted the law which democratically elected politicians should change. There are indeed signs that the German finance ministry is shifting its position, starting even before the pandemic. The new finance minister, Olaf Scholz, appointed a chief economist – Jakob von Weizsacker – who had proposed in 2011 that debt up to 60 per cent of GDP should be pooled among participating countries, with additional debt remaining a national responsibility. Covid-19 pushed Scholz to accept the need for fiscal stimulus and a eurozone package which he claimed, with considerable exaggeration, was Europe’s ‘Hamiltonian moment’. In 1790, Hamilton mutualised existing debt which Scholz’s proposal does not. It does allow joint issuance of debt, but as an emergency measure, and there is no sign that the EU will have major tax-raising powers or a single finance minister. The ‘frugal four’ remain doubtful – and the electoral risks in Germany are high. The proposal might succeed only because it is not a ‘Hamiltonian moment’. At least it is symbolic, as the German deputy finance minister put it, as ‘a significant signal to Europe that we’re serious about the idea of solidarity’.[20]

Solidarity is needed not only in Europe, for even before the

covid-19 crisis there were warning signs of a crisis of debt in emerging and

developing economies, with some countries close to default and unable to borrow

more on international markets. In 2020,

the World Bank worried about ‘a global wave’ of private and public debt in

developing and emerging markets that was fuelled by the savings glut: the level

of debt was higher than in previous waves of indebtedness over the previous 50

years, each of which led to a crisis.[21]

The problem if not only the scale of

debt but a shift in its character. In the 1980s and 1990s,

creditors were banks and governments; now more debt is owned by bond funds who

are reluctant to reschedule and more inclined to hold out. Members of the ‘Paris club’ of official

creditors can negotiate a deal with debtor governments – but the largest

official creditor – China – is not a member and is suspected of using loans to

further its strategic aims. The emerging market debt was an issue before covid-19

and is much more serious and the prospects of international institutions reaching

agreement to prevent another devastating debt crisis and wave of default are

slight given American hostility to multilateral institutions.[22]

The continued implications of policies adopted after the global financial crisis mean that it has not receded into history. Rather, the policies left economies in a fragile position. In Europe and the United States, weak growth and productivity was combined with a savings glut for the rich and debt-funded consumption for the rest, and with an obsession with austerity and the public debt rather than the inequalities that fuelled private indebtedness. The crisis of the eurozone and the need for fiscal transfers was not resolved; and both China and Germany continued to build up savings and surpluses. The need after covid-19 is to adopt policies that were rejected after 2008 in order to provide a better foundation for high and sustainable growth in a green economy where GDP is not at the expense of climate change, and with the benefits more widely distributed.

[1]

Jonathan

Haskel and Sian Westlake, Capitalism Without Capital: The Rise of the

Intangible Economy Princeton and Oxford, 2018; Jim Tomlinson,

‘De-industrialization Not Decline: a New Meta-narrative for Post-war British History’,

Twentieth Century British History 27 (2017), 76-99

[2] George

Parker and Bertrand Benoit, ‘’Berlin Hits Out at “Crass” UK Strategy’, Financial

Times,10 Dec 2008 Adam

Tooze, Crashed: How a Decade of Financial Crises Changed the World

London, 2018, 272-3

[3]

Alberto

Alesina, Carlo Favero and Francesco Giavazzi, Austerity: When it Works and

When It Doesn’t Princeton and Oxford, 2019

[4]

Carmen

Reinhart and Kenneth Rogoff, ‘Growth in a Time of Debt’, NBER Working Paper

15639, Jan 2010

[5]

Barry Eichengreen, Hall of Mirrors: The Great Depression, the Great Recession,

and the Uses – and Misuses – of History New York, 2015, 10.

[6] Oliver

Blanchard and Daniel Leigh, ‘Growth Forecasts and Fiscal Multipliers’, NBER Working

Paper 18779, Feb. 2013

[7]

Nicholas

Crafts, ‘Reducing High Public Debt Ratios: Lessons

from UK Experience’, Fiscal Studies 37 (2016), 201-223; Duncan Needham, ‘Covid-19

and the UK National Debt in Historical Context’, at http://www.historyandpolicy.org/policy-papers/papers/covid-19-and-the-uk-national-debt-in-historical-context

[8] Mark

Blyth, Austerity: The History of a

Dangerous Idea New York, 5, 7, 13-16.

[9] Paul

Krugman, ‘The Third Depression’, New York Times 28 June 2010

[20]

Guy Chazan, ‘The Minds Behind Germany’s Shifting Fiscal Stance’, Financial Times

9 June 2020; Ben Hall, Sam Fleming and Guy Chazan, ‘Is the Franco-German Plan

Europe’s “Hamiltonian” Moment?’, Financial Times, 21 May 2020

[21]

M Ayhan Rose, Peter Nagle, Franziska Ohnsorge and Naotaka Sugawara, Global Waves

of Debt: Causes and Consequences Washington DC: World Bank, 2020

[22]

Colby Smith and Robin Wigglesworth, ‘Why the coming emerging markets debt

crisis will be messy’, FT 12 May 2020; Patrick Bolton, Lee Buchheit,

Pierre-Olivier Gourinchas, Mitu Gulati, Chang-Tai Hsieh, Ugo Panizza and

Beatrice Weder di Mauro, ‘How to Prevent a Sovereign Debt Disaster: A Relief

Plan for Emerging Markets’, at https://www.foreignaffairs.com/articles/world/2020-06-04/how-prevent-sovereign-debt-disaster

http://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.png00Martin Dauntonhttp://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.pngMartin Daunton2020-07-09 09:41:042020-07-09 09:41:06The global financial crisis and Covid-19: learning the lessons

1919 marks the centenary of the founding of the Bauhaus in Weimar by Walter Gropius. The story of his time in London in the 1930s – along with other members of the school – is well worth telling, as it has been in the recent biography by Fiona Macarthy . It is a story about Jack Pritchard and Isokon, of Maxwell Fry and MARS, of the impact of Gropius’s design for Impington Village College on postwar schools. It is part of a wider story of modernist architecture in Britain, such as Berthold Lubetkin’s work for Finsbury – both housing and the health centre. It is a story of hostility but also of postwar influence through Leslie Martin and Eric Lyon’s Span housing. It is a wonderful theme for an exhibition at RIBA, drawing on its own archives and other collections. Sadly, the exhibition fails as a result of the self-indulgent design of Pezo von Ellrichshausen. Plans and documents are hidden in pillars stretching down the exhibition space, glimpsed through circles and triangles at heights that are too high for people who are short and too low for people who are tall, and impossible for anyone in a wheelchair. Reading any of the documents is difficut as a result of shadows and distance. Sofia von Ellrichshausen and Mauricio Pezo are architects based in Chile who are known in Britain for their installation of sixteen steel towers outside Hull Minister, commissioned by RIBA as part of the City of Culture in 2017 which I visited and enjoyed as a witty and playful intervention in what was otherwise a dead space; and for the Sensing Spaces exhibition at the Royal Academy in 2014. They have designed some striking houses. The idiom of their buildings reappears in the exhibition – tower-like structures with irrregular openings – as well as their excellent work in spatial structures that blur the boundary between art and architecture. But they and RIBA have done a disservice to their predecessors, obscuring rather than illuminating the work of Gropius, his fellow exiles and collaborators. They have chosen to make it a self-indulgent exhibition about their own design rather than working in the service of the material or the viewer.

http://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.png00Martin Dauntonhttp://create.martindaunton.co.uk/wp-content/uploads/2019/06/MD-logo.pngMartin Daunton2019-10-06 19:30:422020-07-09 09:36:20Bauhaus and Britain

A shallow history of Brexit could

start with the referendum in June 2016 when 33,577,342 electors voted, with 51.9

per cent opting to leave and 48.1 per cent to remain on a turnout of 72.2 per

cent. It only needed 635,000 of those

voting to change their mind for a different result which was what was widely expected

even by Nigel Farage. Much of the

subsequent debate turned on short-term contingent factors concerning the

campaign – the articulation of the message ‘Take Back Control’, the focus on getting

out people who never voted, the exploitation of the refugee crisis, and the use

of data from Cambridge Analytica and Facebook.

These issues are all Important, and if the vote had gone slightly the

other way, we could not be where we are in 2019.

But focussing on the narrow victory

for leave misses two wider points:

Before the 1975 referendum, British engagement with European integration was distinctive and always differed from the founding members, never fully committed. Why?

There was considerable change since the 1975 referendum when 67.2 per cent were for remain and 32.8 per cent to leave, on a lower turnout of 64.5 per cent. The only two areas with a leave majority were the Western Isles and Shetland. Why this shift since 1975?

These two questions shape a longer or deeper history of the second referendum.

WHY

NOT ENGAGE IN THE INITIAL CREATION OF THE EUROPEAN ECONOMIC COMMUNITY?

Britain’s

circumstances after the war were distinctive and unlike the rest of western

Europe, so that there was rationality in the guarded response to such

initiatives as the European Payments Union and the Coal and Steel

Community. In particular, there were

four features.

Responding to post-war reconstruction

In continental Europe, the experience

at the end of the war offered reasons for integration:

The experience of defeat and occupation led to

a desire to create a stronger bloc to prevent being overwhelmed by the Soviets

and United States

There was a strong sense that the traditional

nation state had failed the people: the recreation of trade for prosperity and welfare

for stability rather than a race to the bottom needed supranational bodies to

work with nation states.

Britain was not defeated or occupied; rather,

the war validated the legitimacy of the state.

There was less concern with being overwhelmed by the United States, and no

reason – as in France or Italy – to fear powerful domestic Communist parties.

Britain did have serious economic

issues that needed to be resolved to which the answer was not European

integration

Debt to US: the end of Lend Lease and the

terms of the post-war loan had conditions attached to end imperial preference

and restore convertibility of the pound

Sterling balances in India, Egypt and

elsewhere had to be paid down

By definition, the defeated or occupied

powers did not owe money to the US and had no accumulated large holdings of

foreign currency overseas – the economic problems at the end of the war were

radically different.

The British government therefore had

different problems, and response to European integration was rational, at least

in the short-term.

Alan Milward rejects the idea that decisions by the British government after the war were blinkered, atavistic or pathological. Rather, they arose from rational thinking about how to adjust to the post-war world. They did not succeed which is not to say they were foolish. British government’s thinking was shaped by two issues: the sterling area and imperial preference..

2. Sterling area

Britain emerged from the war with huge

debts to empire in sterling payments for food, raw material, and military

payments. As a result, sterling formed

about 80 per cent of world reserves, more than before the war: there was a paradox

that the war weakened the British economy but increased sterling’s importance

in global reserves.

These sterling balances were not

convertible into other currencies and were ‘blocked’. There was a major issue of how to deal with

them:

Write them off/down, treat like Lend Lease received

from the United States– some wanted to do this, but it was seen as unwise given

the prospects of independence for India, and the immorality of taking away

accumulated sterling after India suffered so badly from the famine in the war.

Turn the balances into funded debt and pay

interest – but why would holders agree to take a income stream when they wanted to spend the money on

development?

Go for a long, slow grind of paying down

The problem of sterling balances meant

the British government could not engage in the same way as Europeans in the

European Payments Union which was designed to stimulate intra-European trade which

was vital to Europe but less so to Britain given that European markets were

smaller and sterling balances were the major issue.

And there were differences over the

form of European integration – Britain did not welcome a customs unions with

supranational institutions [Saunders 34]

This relates to the other key postwar issue: what to do with imperial preference

3. Imperial preference

Imperial preference was adopted in

1932 in response to the great depression; it formed part of a wider move to

trade blocs throughout the world. In 1930-33, the proportion of imports from

empire rose from 27 to 38 per cent. [O’Rourke]

In 1951, Australia alone took 12 per

cent of British exports – more than the Six founding members of the EEC.

1952-54 Commonwealth took 48 per cent

of exports – Six 19.6 per cent. [Saunders 41]

There is a link with different

policies for agriculture: Britain had a very low proportion in agriculture from

mid-19th century [1871 22.6 per cent when just over 50 per cent in

France], and opted for free trade in food, sold at world price. In the 1930s, the

British government retained this approach through deficiency subsidies to cover

the gap between costs for British farmers and world prices, which were paid by

general taxpayers. In Europe, prices were

kept above world prices by protectionism – hence, support for farmers fell on

consumers. The politics of food and

agriculture radically different

To look beyond Europe was not insular

but a sober though short-sighted appraisal [Saunders 41]

The Six traded mainly with themselves

so the EPU made sense to kick start trade – Britain traded mostly outside Europe, so why disrupt trade

for doubtful benefits?

The Americans wanted Britain to

abandon imperial preference in return for Lend Lease and a post-war loan – but the

British government realised this was not practical.

There was a debate in 1946 over a

European Customs Union: the idea was proposed by Ernie Bevin, foreign

secretary, but opposed by a Cabinet committee led by ministers concerned with

the economy – Hugh Dalton and Stafford Cripps.

The report in 1947 found that a European Customs Union would not be the

best possible outcome for Britain – but if one were formed, Britain should join,

for exclusion would be harmful.

Cabinet agreed to consider an empire

customs union; a combined empire and commonwealth customs union; a European

customs union; and the relationship between the empire and a European customs

union. Meetings to discuss European Customs Union foundered on how to reconcile

with imperial preference [Grob-Fitzgerald 68-9, 75]

A free trade area was more reconcilable

with imperial preference than a customs union: in a free trade area, it would

be possible to have one’s own trade policy (as in NAFTA) and border checks. In a customs union with a common external

tariff, border checks were not needed – but it follows that all goods coming in

from outside had to pay the same tariff, and UK could not offer lower tariffs

to say New Zealand lamb than did France.

Also linked with views on form of cooperation

4. Intergovernmentalism versus supranational institutions

The idea of Commonwealth did not

assume supranational institutions, and Britain obvious had the leading role. The British government would not easily

accept a supranational Europeanism in which it was not the dominant player. The

European Coal and Steel Community – the precursor of the EEC – had a

supranational high authority and court of justice

British preferred the Organisation of European

Economic Cooperation which was an intergovernmental body to divide up Marshall

Aid, exchange information and discuss issues.

Britain did not need to rebuild

institutions after war, did not face issues of collaboration/resistance –

instead, victory in the war enhanced the legitimacy of institutions in a myth

of standing alone against tyranny.

Saunders 40 points out that Britain was with and not of Europe: issues

were discussed with Europe but without an intention of joining in the process

of supranationalism. This was found on

left and right:

On the left, there was concern that

supranationalism wold limit democratic socialism: why nationalise the commanding

heights of coal and steel only to hand them to a European body? Herbert Morrison commented : ‘It’s no good –

the Durham miners won’t wear it’. [Saunders 42]

On the right, there was a sense of global

power. Anthony Eden remarked that ‘Our thoughts move across the seas to the

many communities in which our people play their part, in every corner of the

world. These are our family ties. That

is our life’.

This view was not confined to the

right: Harold Wilson said in 1965 our frontiers are in the Himalayas and that

he would prefer to withdraw half the troops from Germany than any from Far

East.

The British government withdrew from the

Spaak talks in 1955 and devised Plan G of 1956 for an industrial free trade

area under the OEEC. This could maintain

imperial preference and was intergovernmental.

Britain withdrew from European discussions and the treaty of Rome which

had a customs union. Instead, it set up

EFTA in 1960.

Hence thinking about customs union

which is now a key issue in the debate over Brexit goes back to the immediate

post-war period – it was just not seen as significant as it was for European

economies

But by the

1960s, attitudes were changing which takes me to a second question:

WHY

DID ATTITUDES CHANGE SO THAT BRITIAIN JOINED THE EEC WHICH WAS REAFFIRMED IN

1975 REFERENDUM?

In 1971, 244 MPs voted against joining,

356 for. Only 39 Conservatives voted

against the government and against membership – about 80 per cent voted for; 69

Labour MPs voted for membership, against the party line ie about 70 per cent were against.

Pro-European Conservatives wanted the

Commonwealth model but now they had no choice except to enter a body with a

supranational structure; and one with CAP locked in. Why did they accept the change? There were four main reasons.

A wake-up call

The dangers of relying on the sterling